The U.S. healthcare system makes it difficult for patients to plan for ordinary care, let alone a serious illness or emergency. Medical costs are high, insurance rules are complicated, and even people who do everything “right” can still face bills they did not expect and cannot easily afford.

That unpredictability is not incidental. It is structural. The American healthcare system transfers a remarkable amount of financial risk onto patients through premiums, deductibles, denied claims, prior authorization delays, out-of-network charges, prescription costs, and medical debt.

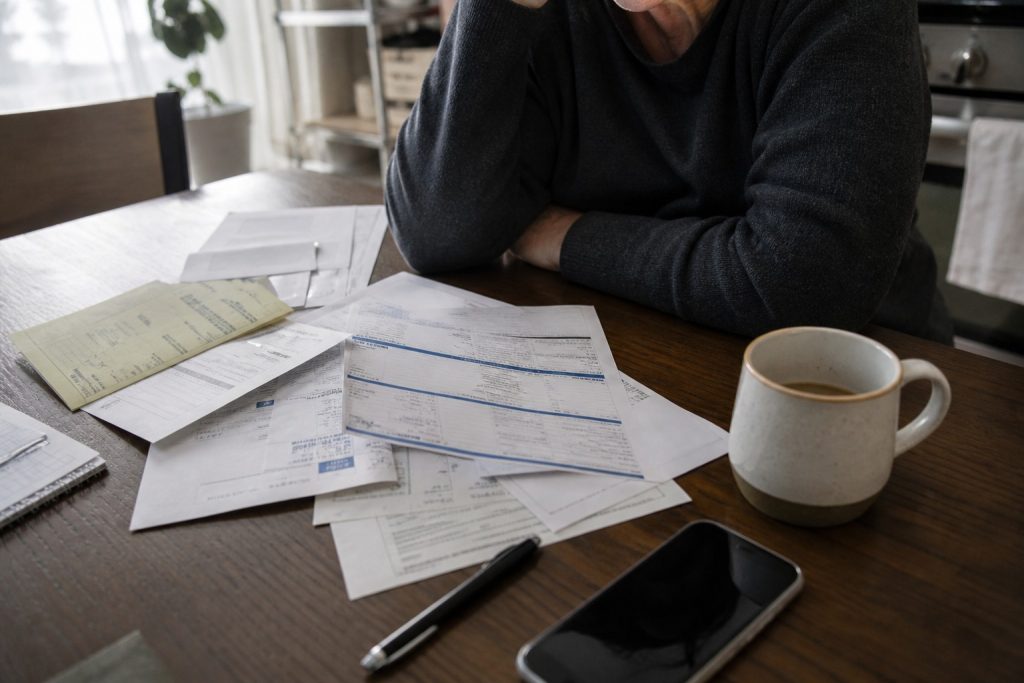

For many households, the result is not just a healthcare problem. It is a financial stability problem. People delay appointments, ration prescriptions, avoid follow-up care, hesitate before calling an ambulance, or take on debt after treatment has already happened.

There are practical ways to reduce the pressure, including payment plans, savings accounts, low-cost clinics, and bill negotiation. But those tools should be understood clearly: they may help patients cope with the system, but they do not fix the deeper problem of unaffordable care.

Key Takeaways

- U.S. healthcare spending is far higher than in comparable wealthy countries, but that spending does not reliably produce better outcomes for patients.

- Insurance can reduce financial risk, but premiums, deductibles, prior authorization, denied claims, and surprise billing gaps still leave patients exposed.

- Medical debt affects millions of Americans, including many people who had insurance when they received care.

- Payment plans can help patients spread costs over time, but they should be treated as a coping tool rather than a real solution to unaffordable healthcare.

- A more sustainable healthcare system would reduce costs and uncertainty at the source, instead of forcing patients to manage the fallout.

The Cost Problem: What Americans Actually Pay

The United States spends more on healthcare per person than any comparable wealthy country. According to the Peterson-KFF Health System Tracker, health spending averaged $14,775 per person in the U.S. in 2024. Switzerland, the next highest-spending comparable country, spent $9,963 per person, while the average among comparable high-income countries was $7,860.

High spending might be easier to defend if it consistently delivered better access, lower stress, and stronger health outcomes. But that is not what international comparisons show. The Commonwealth Fund’s 2024 Mirror, Mirror report ranked the United States last overall among 10 high-income countries, with especially poor performance on access to care, equity, and health outcomes.

For patients, these national numbers show up in everyday ways: premiums, deductibles, copays, coinsurance, prescription costs, specialist bills, and out-of-network charges. Even employer-sponsored insurance, often treated as the more secure form of U.S. coverage, can be expensive. KFF’s 2025 Employer Health Benefits Survey found that the average annual premium for employer-sponsored family coverage reached $26,993, with workers contributing $6,850 on average.

That is before a family has paid many of the other costs that come with using healthcare: a deductible, a hospital bill, a lab fee, a prescription, or time away from work.

Insurance Does Not Mean Protected

Insurance matters. It can make care possible and protect patients from the full price of major treatment. But in the United States, being insured does not always mean being financially safe.

Patients can still face several layers of cost and uncertainty:

- High deductibles: Many patients must pay a substantial amount out of pocket before their insurance covers many services. KFF found that the average deductible among covered workers in plans with a general annual deductible was $1,886 in 2025.

- Prior authorization delays: Insurers may require approval before covering certain medications, scans, treatments, or procedures. The American Medical Association’s 2024 prior authorization survey found that 29% of physicians reported prior authorization had led to a serious adverse event for a patient in their care.

- Surprise billing gaps: The No Surprises Act reduced some unexpected out-of-network bills, especially for emergency and hospital care. But gaps remain. Ground ambulance bills are a major example, with the Commonwealth Fund noting that there are still no federal protections from surprise billing for ground ambulance services.

- Network confusion: A hospital may be in-network while a specialist, lab, or physician group involved in the same episode of care is not. Patients often discover this only after the bill arrives.

This is why healthcare costs feel unstable even to people who have coverage. Patients are not simply deciding whether they can afford a monthly premium. They are trying to predict a chain of costs they may not fully understand until weeks or months after care has already been delivered.

Who Bears the Burden

Healthcare cost instability affects many Americans, but some groups are especially exposed.

- Middle-income households: Middle-class individuals typically don’t qualify for free or low-cost insurance but can’t afford high healthcare and insurance costs.

- Uninsured and underinsured patients: People without coverage face the most obvious risk, but underinsured patients can also face high out-of-pocket costs despite having a plan.

- Patients with chronic illness: Ongoing care means ongoing costs, including appointments, prescriptions, lab work, devices, and specialist visits.

- Black, Hispanic, and lower-wealth households: Medical debt often compounds broader wealth gaps and unequal access to care.

- Rural patients: Fewer provider options, longer travel distances, and limited local services can make care harder and more expensive to access.

The burden is not only about who gets sick. It is also about who has enough savings, flexibility, paid leave, transportation, insurance literacy, and bargaining power to manage the costs that follow.

The Consequences of Financial Instability

When healthcare is financially unpredictable, patients change their behaviour. Some put off routine care. Some delay filling prescriptions. Some avoid follow-up appointments. Others wait until a condition becomes serious enough that they have no choice but to seek help.

Peterson-KFF Health System Tracker data shows that in 2024, about 1 in 6 adults delayed or did not get healthcare because of cost. The same analysis found that 31% of uninsured adults delayed or did not get medical care due to cost, compared with 8% of insured adults.

The consequences can include:

- Care avoidance: Patients skip appointments, tests, dental care, mental health care, or prescriptions because they are worried about the cost.

- Worsening health conditions: Delayed care can allow manageable problems to become more serious, painful, or expensive to treat.

- Medical debt: KFF estimates that people in the United States owe at least $220 billion in medical debt, including roughly 14 million people who owe more than $1,000 and about 3 million who owe more than $10,000.

- Mental health strain: Medical bills can create anxiety, family stress, collection pressure, damaged credit, and the fear that one more health problem could destabilize a household.

Medical debt is often framed as a personal finance issue, but that framing is too narrow. When ordinary care can produce extraordinary bills, debt becomes a predictable outcome of the system itself.

How Payment Plans Are Helping Patients Cope

Because healthcare costs can arrive suddenly, many patients need ways to manage bills after care has already happened. Payment plans can be one of those tools.

A healthcare payment plan allows a patient to spread a bill over time instead of paying the full amount at once. In some cases, a provider may offer a direct, zero-interest arrangement. In others, a third-party financing company may allow patients to apply for structured repayment options. For households with limited cash flow, payment plans can help by easing cash flow without compounding expenses.

That can be genuinely useful. A manageable monthly payment may be less stressful than a large bill due immediately, especially when the alternative is collections or delaying needed care.

But payment plans should be approached carefully. They can make a bill easier to handle in the short term, but they do not make the underlying care affordable. Some medical financing products may include deferred interest, late fees, high interest rates, or terms that are difficult to compare. The Consumer Financial Protection Bureau has warned that medical credit cards and financing plans can carry transparency problems and financial risks for patients.

Before agreeing to a payment plan, patients should ask:

- Is the plan offered directly by the provider or by a third-party lender?

- Is there any interest, deferred interest, late fee, or origination fee?

- What happens if a payment is missed?

- Will the balance be reported to credit agencies?

- Is financial assistance, charity care, or a discount available first?

- Can the provider offer a zero-interest payment arrangement directly?

Patients should also request an itemized bill before committing to repayment. Medical bills can contain errors, duplicate charges, or confusing codes. Asking questions may reduce the balance or reveal assistance options that were not offered upfront.

Other Ways to Make Healthcare More Affordable

Payment plans are only one way patients try to manage healthcare costs. Other strategies may also help, depending on income, insurance status, location, and medical needs.

- Use HSAs and FSAs where available: Health savings accounts and flexible spending accounts allow eligible patients to use tax-advantaged money for qualified medical expenses. They are most useful for people who have enough income to set money aside before costs arise.

- Use preventive care: Many insurance plans cover certain preventive services without cost-sharing. Regular screenings, vaccinations, and checkups can help catch some problems earlier, though prevention cannot eliminate every medical risk.

- Look for community clinics: Federally qualified health centers, nonprofit clinics, public clinics, and university dental schools may offer lower-cost care for uninsured or underinsured patients.

- Ask about financial assistance: Hospitals and nonprofit providers may have charity-care or hardship policies, but patients often need to ask directly and complete paperwork.

- Negotiate or review bills: Patients can request itemized bills, check for errors, ask for discounts, or offer a lower lump-sum payment if they have the means.

These steps can matter. They may reduce immediate harm and help patients avoid the worst financial outcomes. But they are still workarounds. A sustainable healthcare system would not require sick or injured people to become billing investigators, insurance experts, negotiators, and credit-risk analysts just to get care.

Why Reform Is Difficult

Most people can agree that U.S. healthcare is too expensive. The harder question is why the problem persists.

One reason is that healthcare costs are spread across a complicated system of insurers, hospitals, pharmaceutical companies, employers, government programs, providers, billing contractors, and patients. A cost that feels unbearable to a patient may be revenue to another part of the system. That makes reform politically and economically difficult.

There is also the complexity of employer-based insurance. Many Americans receive coverage through work, which means changing jobs, losing hours, becoming self-employed, or leaving the workforce can also change a person’s healthcare situation. This ties medical security to employment in ways that can be especially stressful during illness, caregiving, economic downturns, or major life transitions.

Pricing opacity adds another problem. Patients are often told to be better consumers, but healthcare is not like ordinary shopping. In an emergency, no one is comparing ambulance networks. During surgery, a patient cannot choose every clinician who enters the room. When a doctor recommends a scan or medication, the patient may not know what the insurer will cover or what the final bill will be.

Reform is difficult because the system is not broken in one simple place. It is expensive, fragmented, administratively heavy, and full of competing incentives. But that does not mean patients should be left to manage the consequences alone.

A System Patients Cannot Fix Alone

There are practical steps patients can take. They can review insurance plans carefully, use preventive care when available, ask for itemized bills, apply for financial assistance, consider payment plans cautiously, and seek lower-cost providers where possible.

Those steps can help households survive the system as it exists. They are worth knowing. But they are not proof that the system is working.

Patients did not create the instability of U.S. healthcare, and they cannot solve it by budgeting harder. A sustainable system would reduce costs and uncertainty at the source. It would make care easier to access, bills easier to understand, insurance easier to use, and medical debt less common.

Until then, millions of patients will keep facing the same impossible calculation: whether getting care today will threaten their financial stability tomorrow.